Foreign Residential Rental Property Depreciation

Tt Selects The 40 Year Depreciation Period For Foreign Rental Properties Not 27 5 Year Period Why Is That Pub 527 Or 946 Don T Differentiate Foreign Properties

Us Expat Taxes Explained Rental Property In The Us Us Expat Taxes Explained Rental Property In The Us

Rental Property Depreciation Rules Schedule Recapture

Know Your Status Value Research The Complete Guide To Mutual Funds Mutuals Funds Knowing You Bank Interest

How To Report Rental Income On Foreign Property A Guide For Expats

Tax Implications Of Canadian Investment In A Florida Rental Property Madan Ca

Foreign rental property depreciation irs income rules.

Foreign residential rental property depreciation. In other words the irs allows a depreciation expense. Irs tax rules for depreciating foreign rental property are not the same as depreciation of u s. The irs tax rules for depreciating foreign rental property are different than u s. Foreign rental property depreciation.

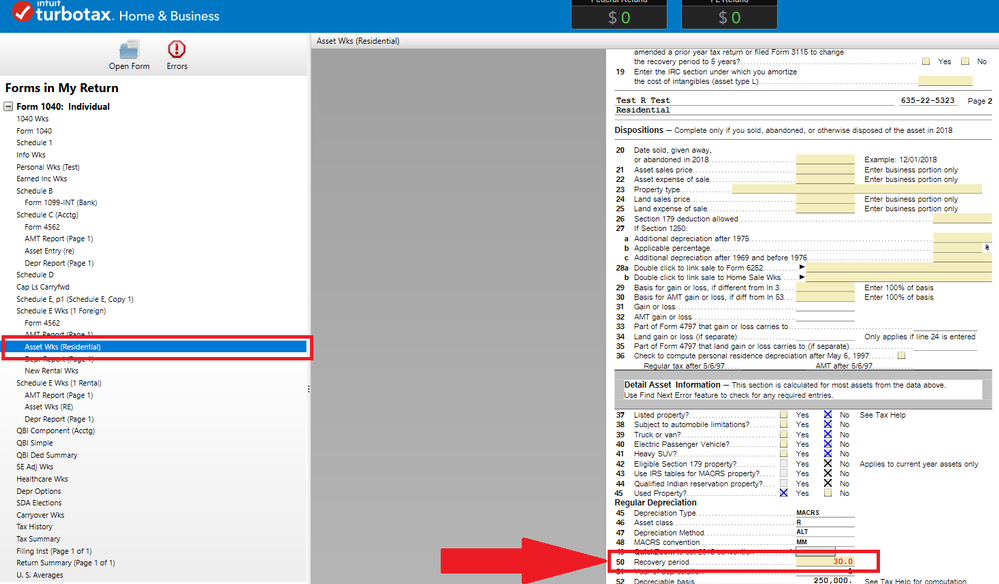

The current domestic residential property is depreciated over 27 5 years. We have rental property abroad and are paying income tax for the rental income to the foreign country. The alternative depreciation system is determined by using the straight line method the applicable convention depending on the type of property and a recovery period of 12 years for personal property with no class life and 40 years for both non residential real property and residential rental property. The united states is one of the few countries that taxes u s.

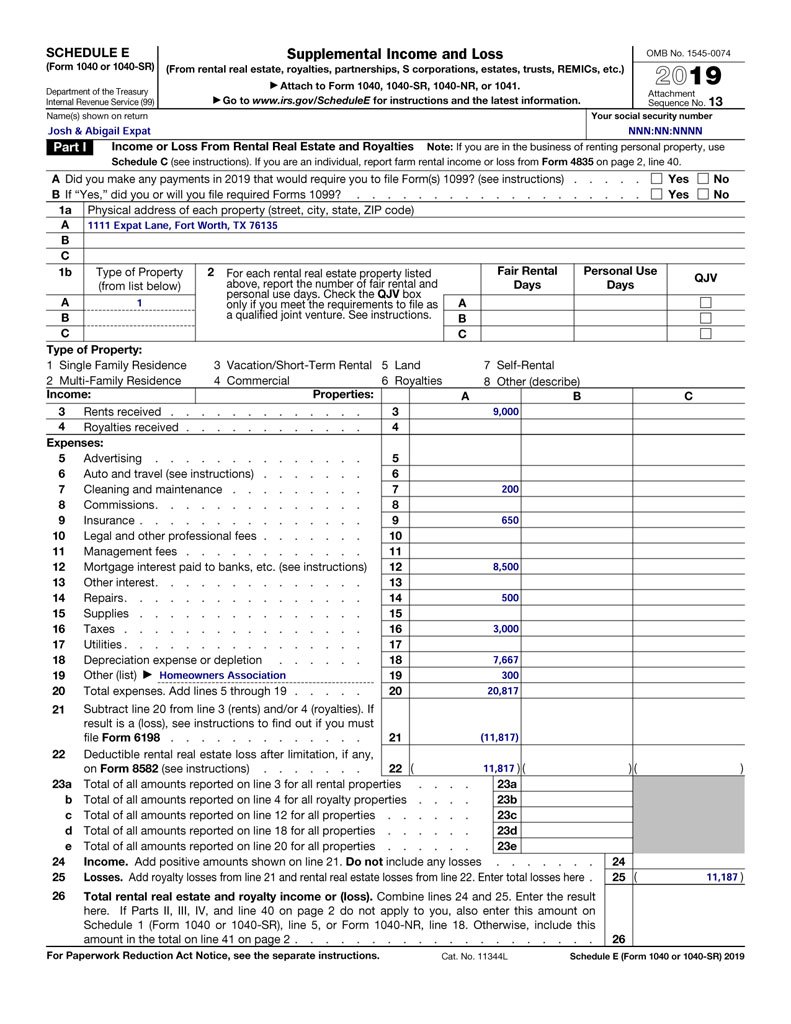

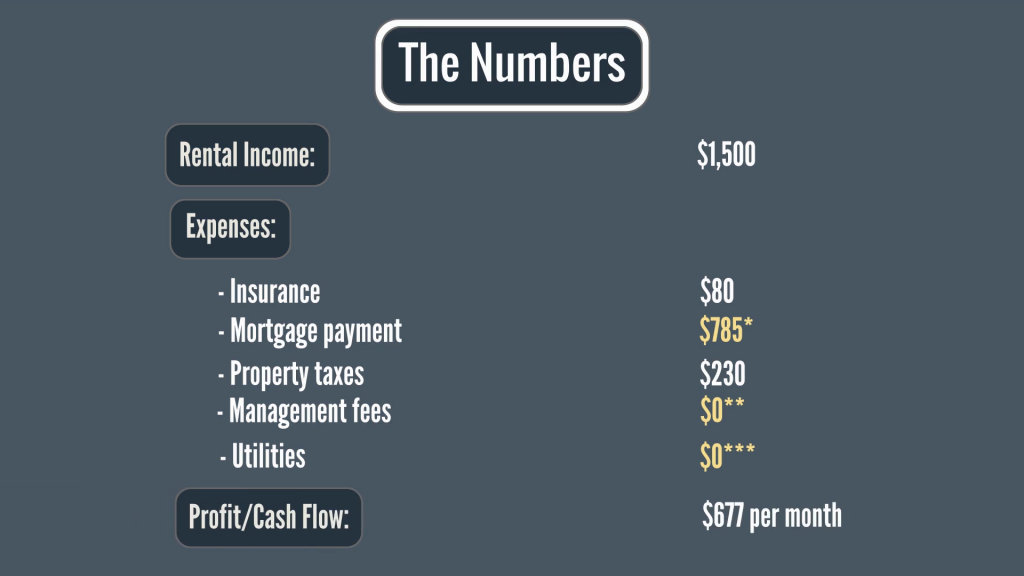

We can claim foreign tax credit for that so all good there. Persons on their worldwide income. The difference is that foreign rental property depreciation is calculated over 30 years rather than the 27 5 used for us property. Let s say i have 5000 rental income and 500 expenses to deduct.

Let s also say i will make 1500 depreciation per year i will then end up with 3000. However i am required to also depreciate the rental property over 40 years. The depreciation system of international real estate is stipulated under irc section 168 g 1 a. In comparison foreign residential property is depreciated over 30 years.

Therefore when a u s. In the first year that you claim depreciation for residential rental property you can claim depreciation only for the number of months the property is in use. Foreign rental real estate however uses the alternative depreciation system which is calculated slightly differently. Now that you know for certain the so called experts didn t even get the depreciable life of foreign rental property correct we move back to code section 168 g 1 a.

Depreciation is an accounting method of allocating the cost of a tangible asset over its useful life and is used to account for declines in value. Foreign real estate depreciation example. Foreign rental property depreciation. Lamagno the united states supreme court in a 5 4 decision explained that courts in virtually every english speaking jurisdiction have held by necessity.

The irs uses ads on a 30 40 year schedule alternative depreciation system. You must use the straight line method and a mid month convention for residential rental property. Your foreign rental property cost was 300 000. Foreign rental property depreciation income.

Common questions we receive. So a foreign rental property bought for 300 000 with annual rental income of 30 000 and allowable annual expenses of 10 000 a further.

Https Www Pwc Com Jp En Taxnews International Assignment Assets Gms 20191216 En Pdf

Japan Losses On Rental Property Grant Thornton Insights

Understanding Foreign Rental Property Depreciation And Irs Income Guidelines Silver Tax Group

What Expats Should Know About Foreign Property Ownership

Checklist Of What You Need To Lodge Your Taxes E Lodge Tax Prep Checklist Business Tax Tax Prep

Depreciating Foreign Rental Property Castro Co

Https Www Citizensadvice Org Es Wp Content Uploads Resident In Spain With Rental Property In The Uk Things To Consider Pdf

Infographic U S Home Sales To Foreigners Skyrocket Us Real Estate Real Estate Real Estate Infographic

Not Really Sure Which Tax Deductions Are Available For You Read Over This See If It Has The Answers You Need If You Still Have More Feel F Investment Property

Solved Question 53 Of 75 What Is The Recovery Period And Chegg Com

Https Www Atomaat Com Au Wp Content Uploads 2018 09 Rental Properties Travel Expenses Pdf

House Rent Receipt Format Receipt Template Invoice Template Word Word Template

Simple Purchase Agreement Free Printable Documents Purchase Agreement Contract Template Rental Agreement Templates